Winter Buyers are Serious

The Ransom-McKenzie Team has been busy already this winter. We’ve been experiencing a high volume of buyers who are ready to buy, now. While winter is often perceived as a down time for real estate, we’re currently seeing trends that indicate this might be a mis-guided perception. Winter buyers are Serious buyers.

Riverside is gorgeous during the winter months!

A recent study of more than 7 million home sales over the past four years revealed that the season in which a home is listed may be able to shed some light on the likelihood that the home will sell for more than asking price, as well as how quickly the sale will close. It’s no surprise that listing a home for sale during the spring saw the largest return, as the spring is traditionally the busiest month for real estate. What is surprising, though, is that listing during the winter came in second!

“Among spring listings, 18.7 percent of homes fetched above asking, with winter listings not far behind at 17.5 percent. While 48.0 percent of homes listed in spring sold within 30 days, 46.2 percent of homes in winter did the same.”

The study goes on to say that:

“Buyers [in the winter] often need to move, so they’re much less likely to make a lowball offer and they’ll often want to close quickly — two things that can make the sale much smoother.”

Bottom Line

If you are debating listing your home for sale within the next 6 months, keep in mind that the spring is when most other homeowners will decide to list their homes as well. Listing your home this winter will ensure that you have the best exposure to the serious buyers who are out looking now! The study used the astronomical seasons to determine which season the listing date fell into (Winter: Dec. 21 – Mar. 20; Spring: Mar. 21 – June 20; Summer: June 21 – Sept 21; Autumn: Sept 21 – Dec. 20).

Millenials vs Boomers

According to the Census Bureau, millennials have overtaken baby boomers as the largest generation in U.S. History. Millennials, or America’s youth born between 1982-2000, now represent more than one quarter of the nation’s population, totaling 83.1 million. There has been a lot of talk about how, as a generation, millennials have ‘failed to launch’ into adulthood and have delayed moving out of their family’s home. Some experts have even questioned whether or not millennials want to move out. The great news is that not only do millennials want to move out… they are moving out! The National Association of Realtors (NAR) recently released their 2016 Profile of Home Buyers and Sellers in which they revealed that 61% of all first-time home buyers were millennials in 2015! The median age of all first-time buyers in 2015 was 31 years old. Here is chart showing the breakdown by age:

If you recall from one of our posts last week, first time home buyers comprised 33% of all buyers in October 2016. The above chart gives you an idea as to how many of those buyers are from the younger generation. Many social factors have contributed to millennials waiting to buy their first home. The latest Census results show that the median age of Americans at the time of their first marriage has increased significantly over the last 60 years, from 23 for men & 20 for women in 1955, to 29 & 27, respectively, in 2015. Those who went to college and took out student loans are finally paying them off, as the terms on traditional student loans are 10 years. This means that a large portion of the generation is making its last loan payments and is working toward saving for a first home. As a whole, the first-time home buyer share increased to 35% of all buyers, up from 32% in 2014. Not all millennials are first-time buyers, they also made up 12% of all repeat buyers!

Bottom Line

Millennials will continue to drive the housing market next year, as well as in the years to come. As more and more realize that owning a home is within their grasp, they will flock to own their piece of the American Dream. Are you ready to buy your first or even second home? Give the Ransom-McKenzie Team a call and we’ll help you through the process.

Interest Rates Going UP in 2017

According to Freddie Mac’s latest Primary Mortgage Market Survey, the 30-year fixed rate mortgage interest rate jumped up to 3.94% shortly after the election last month. Interest rates had been hovering around 3.5% since June, and many are wondering why there has been such a significant increase so quickly.

Why did rates go up?

Whenever there is a presidential election, there is uncertainty in the markets as to who will win. One way that this is noticeable is through the actions of investors. As we get closer to the first Tuesday of November, many investors pull their funds from the more volatile and less predictive stock market and instead, choose to invest in Treasury Bonds. When this happens, the interest rate on Treasury Bonds does not have to be as high to entice investors to buy them, so interest rates go down. Once the elections are over and a President has been elected, investors return to the stock market and other investments, leaving the Treasury to raise rates to make bonds more attractive again. Simply put, the better the economy, the higher interest rates will go. For a more detailed explanation of the many factors that contribute to whether interest rates go up or down, you can follow this link to Investopedia.

The Good News

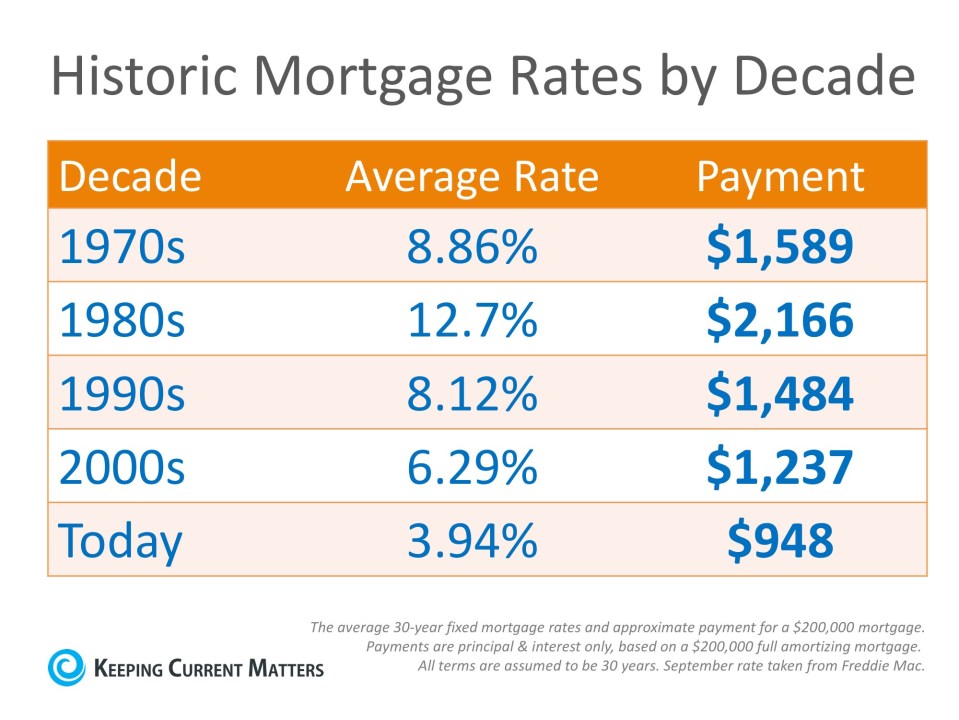

Even though rates are closer to 4% than they have been in nearly 6 months, they are still slightly below where we started 2016, at 3.97%. The great news is that even at 4%, rates are still significantly lower than they have been over the last 4 decades, as you can see in the chart below.

Any increase in interest rate will impact your monthly housing costs when you secure a mortgage to buy your home. A recent Wall Street Journal article points out that, “While still only roughly half the average over the past 45 years, according to Freddie Mac, the quick rise has lenders worried that home loans could become more expensive far sooner than anticipated.” Tom Simons, a Senior Economist at Jefferies LLC, touched on another possible outcome for higher rates:

“First-time buyers look at the monthly total, at what they can afford, so if the mortgage is eaten up by a higher interest expense then there’s less left over for price, for the principal. Buyers will be shopping in a lower price bracket; thus demand could shift a bit.”

Bottom Line

Interest rates are impacted by many factors, and even though they have increased recently, rates would have to reach 9.1% for renting to be cheaper than buying. Rates haven’t been that high since January of 1995, according to Freddie Mac.

The Ransom-McKenzie Team is here to help you through all of the details involved in buying or selling a home. Give us a call today and let us help you!

Home Sales Continue UP

People often ask us how the world of real estate is doing in Riverside. Especially now that we’re closing in on another year, and are looking into next year with a new Presidential administration. We can honestly say that we have had a great 2016, and we are looking forward to more sales in 2017.

The most telling fact in this infographic is that nationwide we’re still experiencing low inventory. While this is driving sales, and has made October the 56th month that we have experienced year-over-year price gains, it has not been pushing prices up as high as one might think. According to the Inland Valleys Association of Realtors Housing Data Report for October 2016 the median sales price in Riverside is $345,000 which is an increase of 5.8% from the previous year. This shows that we are experiencing steady growth in our marketplace.

A nationwide fun fact is that currently 33% of home buyers in October 2016 were first-time home buyers. This shows that the American Dream of home ownership is continuing to be important into the next generation.

The Ransom-McKenzie Team looks forward to assisting our friends and clients with their real estate needs as we look forward to the coming new year. Give us a call if you have a questions about buying or selling a home in Riverside. We Love Riverside!

Happy Mother’s Day!

As families celebrate Mother’s Day across the country, I’m preparing for an open house at one of our new listings. I know it seems like it is a bummer to have to “work” Mother’s Day, but somehow it doesn’t seem so bad. Mostly because Connie is my mother!

It is a pleasure and a privilege to be able to work with my mother every day. Not everyone is lucky enough to have such a strong relationship with their mother. It is what makes the Ransom-McKenzie Team strong.

Join us today at our Open House from 1-4pm at 1367 Ransom Road. We look forward to seeing you there. We’ll even have a surprise for the mothers who stop by!!

Check out our video tour of 1367 Ransom Road!

Happy Mother’s Day!!

Sales Price vs. Appraised Value

The Ransom-McKenzie Team is often contacted by sellers who are interested in determining the value of their home. In many instances, they already have a number in mind, they are just looking for us to validate their price. Sometimes we come in with a price at or close to what the seller’s believe to be the value of their home….. other times we don’t. When you are listing your home for sale, choosing the right listing price is an important part of the process for a number of reasons. The most important of those reasons is to make sure that your sales price is going to match the appraiser’s valuation of the home.

The Sales Price

Of course, most sellers want to maximize the value they get for the house. However, the price they set might not be reflective of the other comparable homes in the neighborhood. A recent post on “The Home Story”, a site published by Fannie Mae, explained the difference between the price a seller may get for their home and the value an appraiser might assign the property. The article starts out by stating a fact which is all too familiar to Realtors:

“People tend to view their homes emotionally, and that can become quickly apparent when they decide to sell.”

Nice presentation can positively affect a sale price, but is not the only deciding factor.

That doesn’t mean that the home won’t necessarily sell for that price. A seller can set an asking price and actually have a buyer agree to that price. However, that value may not be necessarily in agreement with what most buyers are willing to pay. For example, one person can view a property, determine it is exactly what they are looking for and well worth the asking price, whereas another person could look at the same property and feel the asking price is too high. Steven Corbin, Director of Valuation in Fannie Mae’s CPM Real Estate division gives an example of this scenario:

“Someone may have driven by the property countless times, and they really want to live in that house. So in reality they may overbid for that property. This would be a situation where the actions of a specific buyer do not represent the actions of a typical buyer.”

The Appraised Price (Market Value)

In their article Fannie Mae describes the process used to determine the value of a home to satisfy their determination of value:

“When a contract is established on a property, an appraised value is determined by a professional real estate appraiser. The appraiser works on the lender’s behalf to determine that value by taking many factors into consideration, including the neighborhood, the value of properties of similar size and construction, and even such things as the type of fixtures on the premises and layout of the floor plan.”

The bank, or lender, wants to know the value that a typical buyer would pay for the property. This price may differ from the agreed upon sales price that the seller and buyer had in the contract.

Selling Your Home Twice

The fact is, when you’re selling your home, you actually have to sell it twice. The first sale occurs when you get the right buyer and all parties agree upon a price. The second sale, which often is the more challenging of the two, is to get the bank, (aka the appraiser), to agree to the same value. If the appraiser comes in with a value that is below the agreed upon sales price, the lending institution might not authorize the mortgage for the full amount a buyer would need to complete the transaction. Quicken Loans actually releases a Home Price Perception Index (HPPI) that quantifies the difference between what sellers and appraisers believe regarding value. The HPPI represents the difference between appraisers’ and homeowners’ opinions of home values. Currently, there is approximately a 2% difference between what homeowners believe their home to be worth and what appraisers value that same home. On a $300,000 sale that would be a $6,000 difference. That could be a challenge that might prevent the home sale proceeding to the closing table.

Bottom Line

In a housing market like the one we’re experiencing in the City of Riverside right now, where supply is very low and demand is very high, home values can increase rapidly. One major challenge in such a market is the bank appraisal. If prices are jumping, it is difficult for appraisers to find adequate comparable sales (similar houses in the neighborhood that closed recently) to defend the price when performing the appraisal for the bank. With escalating prices, the second sale might be even more difficult than the first. That is why we suggest that you use an experienced real estate professional to help set your listing price. Call the Ransom-McKenzie Team today to discuss the value of your home. We’ll be happy to assist you with every step of your real estate transaction.

A+ Real Estate Facts

Some Highlights:

- Hiring a Real Estate Professional to buy your dream home, or sell your current house is one of the most ‘educated’ decisions you can make!

- A Real Estate Professional has the experience needed to help you through the entire process.

- Make sure that you hire someone who knows current market conditions & can simply & effectively explain them to you & your family!

High Foot Traffic = Hot Home Sales

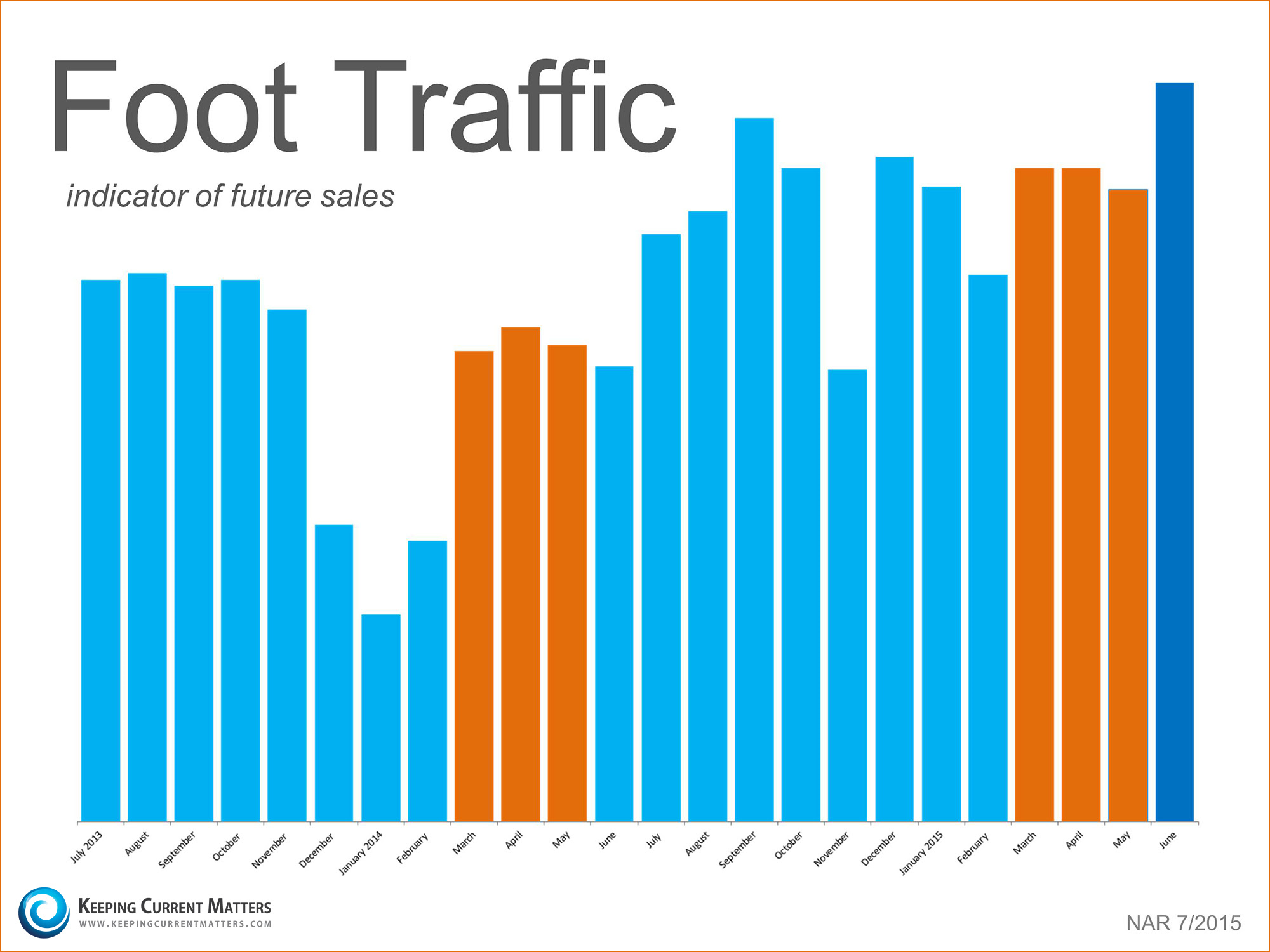

Getting traffic through your home when it is for sale is always a key component to getting the home sold. Foot Traffic is also an indicator used to predict the strength of the real estate market. Guess what? This summer is proving to be a hot real estate season.

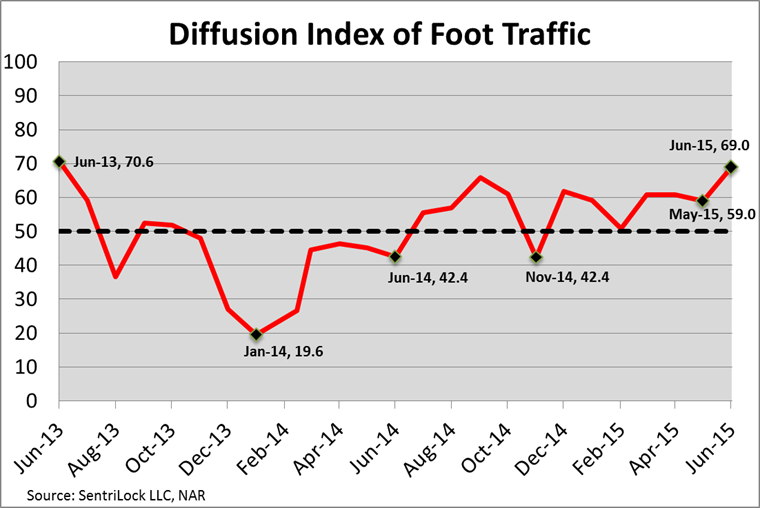

The National Association of Realtors (NAR) publishes a monthly “Foot Traffic Report“, (yes, there is such a thing), which tracks traffic through homes on the market. This tracking is done through the electronic locks that Realtors use to access keys to show homes. It represents the number of homes that have been shown by a realtor. Looking at the graph below it is apparent that there is a strong uptick in the number of showings just in the last 2-3 months.

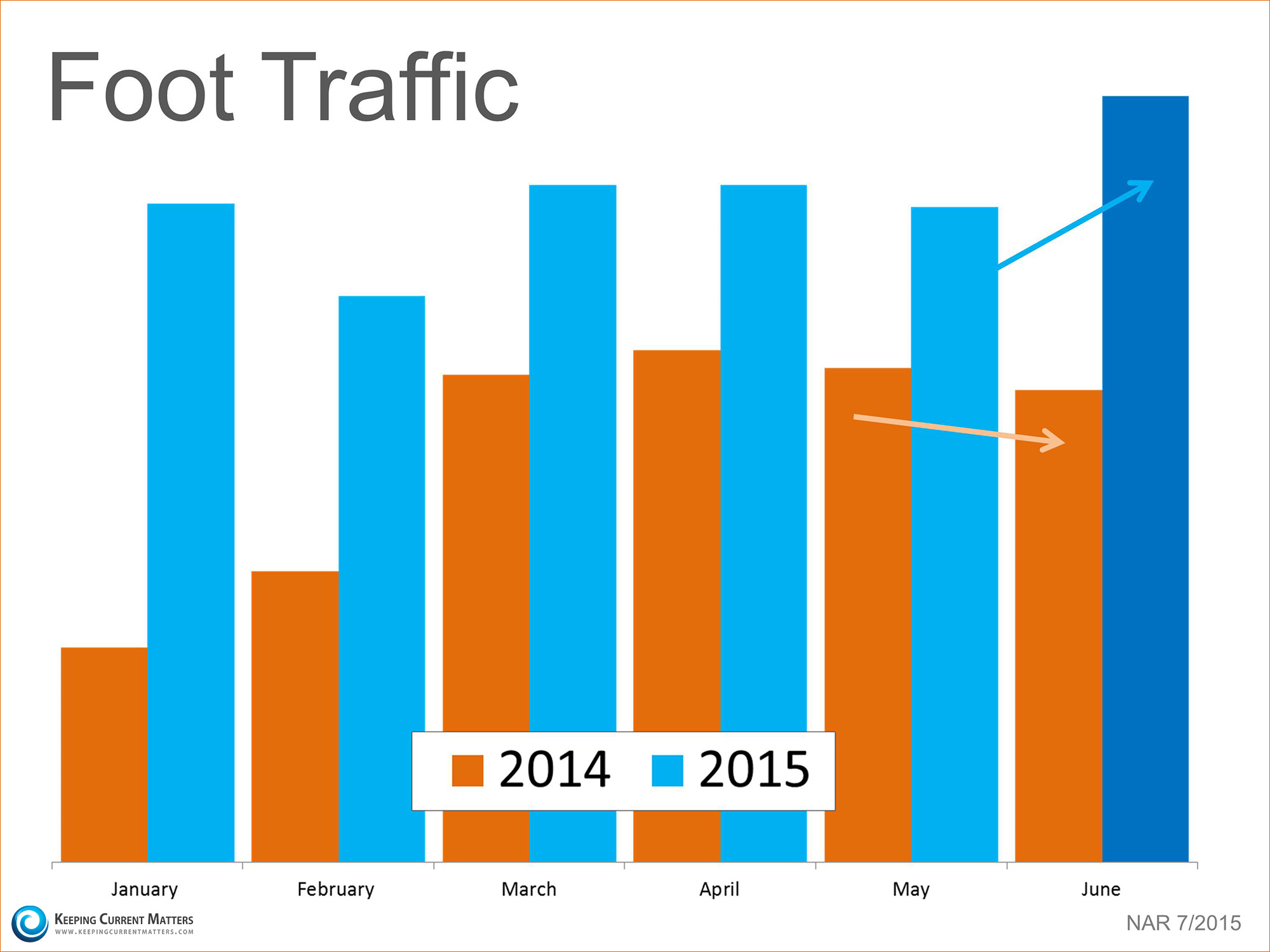

People always talk about the “spring buying season” when they talk real estate. However, this year it appears as though the summer real estate market will be just as hot. NAR’s most recent “Foot Traffic Report” revealed that there are more buyers out looking at homes right now than at any other time in the last two years including the past two springs (in orange below). Remember, this is just Relator showings, it does not include other traffic such as open houses, which have also been very busy as well recently.

The Foot Traffic Report is compiled from data on the number of properties shown by Realtors. NAR further explains:

“Foot traffic has a strong correlation with future contracts and home sales, so it can be viewed as a peek ahead at sales trends two to three months into the future.”

We can see that the number of prospective purchasers out looking at homes has been greater each month this year compared to the same month in 2014. And, though foot traffic fell off last June as compared to May, this year it has increased nicely.

The bottom line is that the housing market will remain strong throughout the summer and into the fall, making for one of the best years in real estate over the last decade. If you’re on the fence as to whether or not you want to list your home, give the Ransom-McKenzie Team a call. We would be happy to meet with you to discuss the market in Riverside and assist you with your Real Estate needs.

The bottom line is that the housing market will remain strong throughout the summer and into the fall, making for one of the best years in real estate over the last decade. If you’re on the fence as to whether or not you want to list your home, give the Ransom-McKenzie Team a call. We would be happy to meet with you to discuss the market in Riverside and assist you with your Real Estate needs.

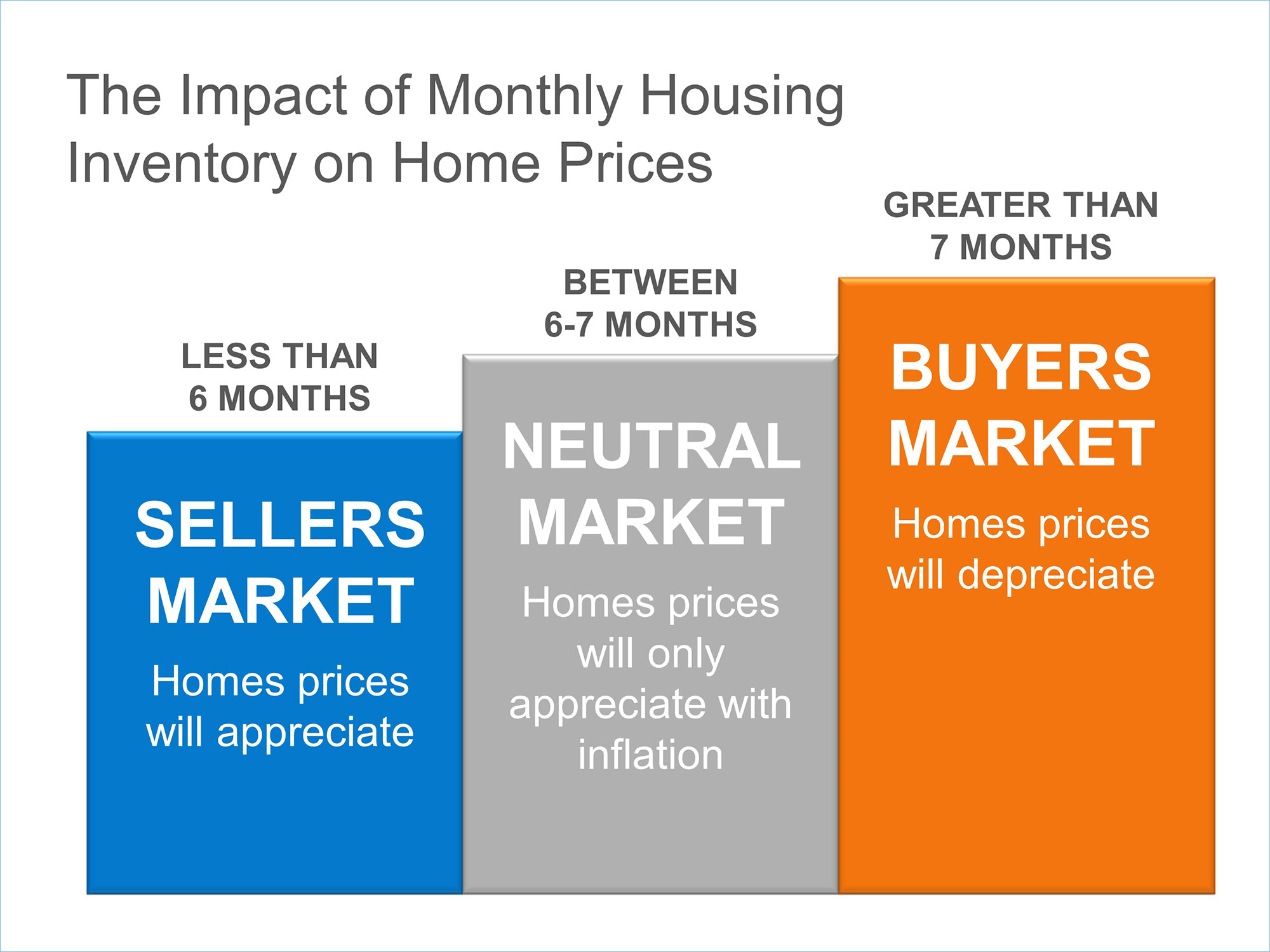

Home Inventory Logic

If you are one of the many homeowners out there who are debating putting their house on the market this year, don’t miss out on the great opportunity you have right now!

The latest Existing Home Sales Report from The National Association of Realtors (NAR), reveals that the inventory of homes for sale has dropped to a 5.1-month supply. Historically, a 6-month supply is necessary for a ‘normal’ market, as explained below:

There are more buyers that are ready, willing and able to buy now, than there has been in years! The supply of homes for sale is not keeping up with the demand of these buyers. We are experiencing this shortage of inventory in Riverside as well. According to Lawrence Yun, Chief Economist for NAR, the most recent numbers available show that solid sales gains are being seen for May 2015 figures. However, he also noted that:

“Overall supply still remains tight, homes are selling fast and price growth in many markets continues to teeter at or near double-digit appreciation. Without solid gains in new home construction, prices will likely stay elevated — even with higher mortgage rates above 4 percent.”

With the average number of days on the market at less than a month, right now is an excellent time to list your home. Our inventory in Riverside is below the 5 month mark so we are most definitely in a seller’s market. Listing your home now will give you the most exposure to buyers who will be competing against each other to buy your home.

Call the Ransom-McKenzie Team today to help you navigate through the process of selling or buying your home. We have the experience you’ll need to make the process as stress free as possible.

Save the Date Riverside!

As we look at more sustainable ways of living, the idea of solar energy becomes more enticing every day. But, solar technology is changing rapidly. How do we know what is the best option for us in our homes, or for our businesses?

One way to learn more is to attend UCR’s second conference on solar energy. Opportunities for Solar: Ways Forward for Inland Southern California on September 30, 2015.

This conference is a collaborative effort put together by the Center for Environmental Research & Technology: CE-CERT EVENTS, Bourns College of Engineering Center for Environmental Research and Technology, the Center for Sustainable Suburban Development, and the Southern California Research Initiative for Solar Energy.

This conference is designed to inform attendees of the importance of solar energy and to discuss the latest technology, public policy & regulations, economic impacts, and opportunities for incorporating solar energy into our daily lives in the Inland Southern California region. The Directors of CE-CERT state in a letter on the conference website that,

We believe solar energy can play a significant role in the region’s future, not only because of the abundance of sunlight afforded to the region and its potential as another source of efficient and cost effective energy, but as an integral contributor to Inland Southern California’s employment base.

The Inland Empire, and specifically the City of Riverside, is home to a number of solar industry leaders and innovators who will be participating in this conference. Registration for the conference starts soon. Early bird registrants will pay $50 to attend the all day conference. For more information regarding registration, speakers & sponsors, or to participate in the conference, visit the CE-CERT webpage.