69% of New Homebuyers are Wrong About Down Payment Needs

According to a recent survey conducted by Genworth Financial Inc. at the Annual Mortgage Bankers’ Association Secondary Market Conference, 69% of potential first-time buyers still believe a 20% down payment is necessary to buy in today’s market.

Nearly 40% of mortgage industry professionals surveyed believe that a lack of knowledge about the home-buying process is keeping potential buyers on the sidelines. Saving for a down payment is often cited as a huge barrier for first-time homebuyers to make the leap into homeownership. If homeowners believe that they need a 20% down payment to enter the market, they also believe that they will have to wait years (in some markets) to come up with the necessary funds to buy their dream homes. The greatest source of confusion cited in the survey results centered around down payments. The results are broken down in the chart below.

Rohit Gupta, CEO of Genworth Mortgage Insurance had this to say,

“While first-time homebuyers continue to drive the purchase market, we believe many are staying on the sidelines due to the misconception that a 20 percent down payment is required to secure a mortgage. There are various low down payment options available today that allow prospective homebuyers to reach their dreams of homeownership sooner. It is crucial that, as an industry, we proactively educate eligible borrowers about solutions that will enable them to buy a home when they’re ready.”

Bottom Line

Don’t let a lack of understanding of the home-buying process keep you and your family out of the housing market. Give the Ransom-McKenzie Team a call to day to help you understand the local Riverside Real Estate Market.

Happy Memorial Day!

ALL GAVE SOME, SOME GAVE ALL

Today we honor and remember all of the patriots who sacrificed their lives in service to our Country. To those heroes and their families, we are eternally grateful.

____________________________________________________________________________________________

Inventory Shortage is Slowing Sales

The real estate market is moving more and more into a complete recovery. Home values are up. Home sales are up. Distressed sales (foreclosures and short sales) have fallen dramatically. It seems that 2017 will be the year that the housing market races forward again. However, there is one thing that may cause the industry to tap the brakes: a lack of housing inventory. While buyer demand looks like it will remain strong throughout the summer, supply is not keeping up. Here are the thoughts of a few industry experts on the subject:

Lawrence Yun, Chief Economist at NAR:

“Sellers are in the driver’s seat this spring as the intense competition for the few homes for sale is forcing many buyers to be aggressive in their offers. Buyers are showing resiliency given the challenging conditions. However, at some point — and the sooner the better — price growth must ease to a healthier rate. Otherwise sales could slow if affordability conditions worsen.”

Tom O’Grady, Pro Teck CEO

“The lack of inventory is very real and could have a severe impact on home sales in the months to come. Traditionally, a balanced market would have an MRI (Months Remaining Inventory) between six and 10 months. This month, only eight metros we track have MRIs over 10, compared to 27 last year and 48 two years ago—illustrating that this lack of inventory is not being driven by traditionally ‘hot’ markets, but is rather a broad-based, national phenomenon.”

Ralph McLaughlin, Chief Economist at Trulia

“Nationally, housing inventory dropped to its lowest level on record in 2017 Q1. The number of homes on the market dropped for the eighth consecutive quarter, falling 5.1% over the past year.”

Freddie Mac

“Tight housing inventory has been an important feature of the housing market at least since 2016. For-sale housing inventory, especially of starter homes, is currently at its lowest level in over ten years. If inventory continues to remain tight, home sales will likely decline from their 2016 levels. …all eyes are on housing inventory and whether or not it will meet the high demand.”

Bottom Line

If you are thinking of selling, now may be the time. Demand for your house will be strongest at a time when there is very little competition. That could lead to a quick sale for a really good price. The Ransom-McKenzie Team can help you with market data, and the best tools to get your home sold quickly. Give us a call today or visit our website at Ransom-McKenzie.com for market insights.

Real Estate Lingo Guide for Buyers

Buying a home can be intimidating if you are not familiar with the terms used during the process. To start you on your path with confidence, we have compiled a list of some of the most common terms used when buying a home. Freddie Mac has compiled a more exhaustive glossary of terms in their “My Home” section of their website.

Annual Percentage Rate (APR) – This is a broader measure of your cost for borrowing money. The APR includes the interest rate, points, broker fees and certain other credit charges a borrower is required to pay. Because these costs are rolled in, the APR is usually higher than your interest rate.

Appraisal – A professional analysis used to estimate the value of the property. This includes examples of sales of similar properties. This is a necessary step in getting your financing secured as it validates the home’s worth to you and your lender.

Closing Costs – The costs to complete the real estate transaction. These costs are in addition to the price of the home and are paid at closing. They include points, taxes, title insurance, financing costs, items that must be prepaid or escrowed and other costs. Ask your lender for a complete list of closing cost items.

Credit Score – A number ranging from 350-800, that is based on an analysis of your credit history. Your credit score plays a significant role when securing a mortgage as it helps lenders determine the likelihood that you’ll repay future debts. The higher your score, the better, but many buyers believe they need at least a 780 score to qualify when, in actuality, over 55% of approved loans had a score below 750.

Discount Points – A point equals 1% of your loan (1 point on a $200,000 loan = $2,000). You can pay points to buy down your mortgage interest rate. It’s essentially an upfront interest payment to lock in a lower rate for your mortgage.

Down Payment – This is a portion of the cost of your home that you pay upfront to secure the purchase of the property. Down payments are typically 3 to 20% of the purchase price of the home. There are zero-down programs available through VA loans for Veterans, as well as USDA loans for rural areas of the country. Eighty percent of first-time buyers put less than 20% down last month.

Escrow – The holding of money or documents by a neutral third party before closing. It can also be an account held by the lender (or servicer) into which a homeowner pays money for taxes and insurance.

Fixed-Rate Mortgages – A mortgage with an interest rate that does not change for the entire term of the loan. Fixed-rate mortgages are typically 15 or 30 years.

Home Inspection – A professional inspection of a home to determine the condition of the property. The inspection should include an evaluation of the plumbing, heating and cooling systems, roof, wiring, foundation and pest infestation.

Mortgage Rate – The interest rate you pay to borrow money to buy your house. The lower the rate, the better. Interest rates for a 30-year fixed rate mortgage have hovered between 4 and 4.25% for most of 2017.

Pre-Approval Letter – A letter from a mortgage lender indicating that you qualify for a mortgage of a specific amount. It also shows a home seller that you’re a serious buyer. Having a pre-approval letter in hand while shopping for homes can help you move faster, and with greater confidence, in competitive markets.

Primary Mortgage Insurance (PMI) – If you make a down payment lower than 20% on your conventional loan, your lender will require PMI, typically at a rate of .51%. PMI serves as an added insurance policy that protects the lender if you are unable to pay your mortgage and can be cancelled from your payment once you reach 20% equity in your home. For more information on how PMI can impact your monthly housing cost, click here.

Real Estate Professional – An individual who provides services in buying and selling homes. Real estate professionals are there to help you through the confusing paperwork, to help you find your dream home, to negotiate any of the details that come up, and to help make sure that you know exactly what’s going on in the housing market. Real estate professionals can refer you to local lenders or mortgage brokers along with other specialists that you will need throughout the home-buying process.

The best way to ensure that your home-buying process is a confident one is to find a real estate professional who will guide you through every aspect of the transaction with ‘the heart of a teacher,’ and who puts your family’s needs first. The Ransom-McKenzie Team are here to help you. Visit our website at http://www.ransom-mckenzie.com to learn more about buying your dream home.

Inventory Shortage = Inventory Mismatch

The inventory of existing homes for sale in today’s market was recently reported to be at a 3.6 month supply according to the National Association of Realtors latest Existing Home Sales Report. Inventory is now 7.1% lower than this time last year, marking the 20th consecutive month of year-over-year drops.

Historically, inventory must reach a 6 month supply for a normal market where home prices appreciate with inflation. Anything less than a 6 month supply is a sellers’ market, where the demand for houses outpaces supply and prices go up. As you can see from the chart below, the United States has been in a sellers’ market since August 2012, but last month’s numbers reached a new low.

We’ve seen this trend in the Riverside market as we continue to hope that more homes will come on the market each month. One of the unusual things about this market though is that home prices are not skyrocketing. They are increasing, yes, but not the way the economic tables tell us they should be. Why is this? We found this interesting explanation in today’s Keeping Current Matters blog offering.

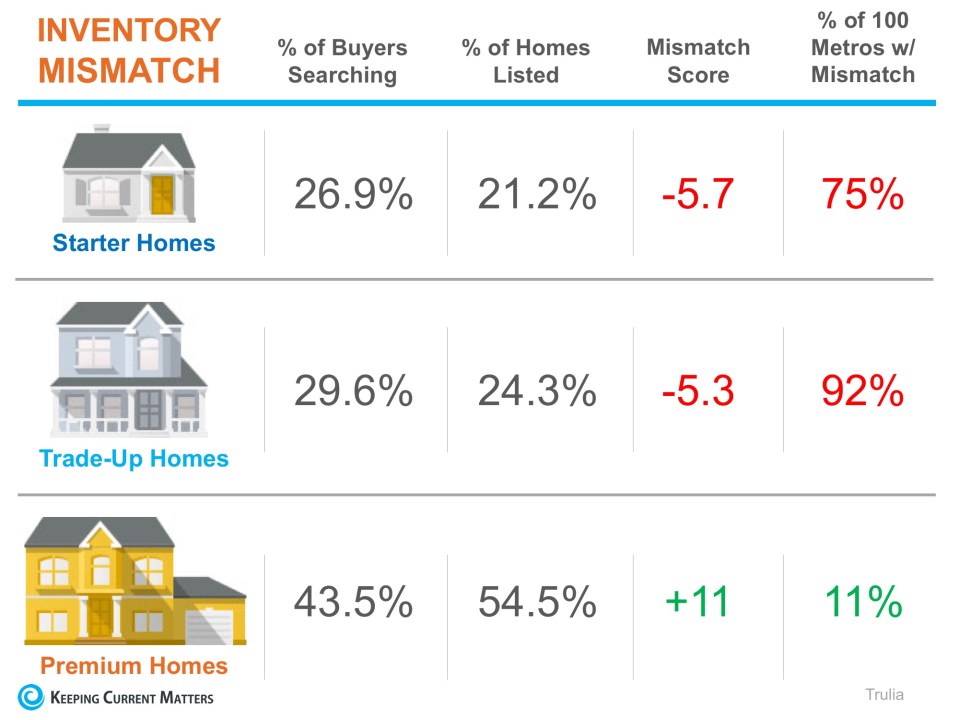

Recently Trulia revealed that not only is there a shortage of homes on the market in general, but the homes that are available for sale are not meeting the needs of the buyers that are searching.

Homes are generally bucketed into three groups by price range: Starter, Trade-Up, and Premium.

Trulia’s market mismatch score measures the search interest of buyers against the category of homes that are available on the market. For example: “if 60% of buyers are searching for starter homes but only 40% of listings are starter homes, [the] market mismatch score for starter homes would be 20.”

The results of their latest analysis are detailed in the chart below.

Nationally, buyers are searching for starter and trade-up homes and are coming up short with the listings available, leading to a highly competitive seller’s market in these categories. Ninety-two of the top 100 metros have a shortage in trade-up inventory. Riverside is one of these areas as well. Trade-up inventory, especially if the buyer is looking for a single story home, is very hard to come by.

Premium home buyers have the best chance of less competition and a surplus of listings in their price range with an 11-point surplus, leading to more of a buyer’s market.

“It leaves Americans who are in the market for a home increasingly chasing too fewer options in lower price ranges, and sellers of premium homes more likely to be left waiting longer for a buyer.”

Lawrence Yun, NAR’s Chief Economist doesn’t see an end to this coming any time soon:

“Competition is likely to heat up even more heading into the spring for house hunters looking for homes in the lower- and mid-market price range.”

What Should You Do?

Real estate is local. If you are thinking about buying OR selling this spring in Riverside, sit with a local real estate professional who can share with you the exact market conditions in your area. The Ransom-McKenzie Team lives and works in Riverside. We can help you to understand the local market, and advise you on how to move forward with your selling or buying plans. Give us a call today at 951-237-2044.

Thinking of Selling? Do it TODAY!

| That headline might be a little aggressive. However, as the data on the 2017 housing market begins to roll in, we can definitely say one thing: If you are considering selling,

IT IS TIME TO LIST YOUR HOME!

The February numbers are not in yet, but the January numbers were sensational. Lawrence Yun, Chief Economist for the National Association of Realtors, said:

And CNBC says consumer confidence in the economy is fueling the market:

The only challenge to the market is a severe lack of inventory. A balanced market would have a full six-month supply of homes for sale. Currently, there is less than a four-month supply of inventory. This represents a decrease in supply of 7.1% from the same time last year. With demand increasing and supply dropping, this may be the time to get the best price for your home. The much anticipated interest rate hike in the coming weeks has made buyers ready to buy NOW! Give the Ransom-McKenzie Team a call to discuss what your home might sell for. We look forward to helping you with your real estate needs in Riverside. |

Reality TV: Myth v.s. Real Life

| Have you ever been flipping through the channels, only to find yourself glued to the couch in an HGTV binge session? We’ve all been there… watching entire seasons of “Love it or List it,” “Fixer Upper,” “House Hunters,” “Property Brothers,”and so many more, just in one sitting. When you’re in the middle of your real estate themed show marathon, you might start to think that everything you see on TV must be how it works in real life, but you may need a reality check.

We’re finding more and more that buyers and sellers expect their real estate experience to be just like they see on the popular reality TV shows. Buyers want the homes to be perfect, updated and priced perfectly. Sellers want to sell the home at the first open house and believe that their home should be priced above market so they can get an offer close to where they want it to be sold. This is not always the case. Reality TV Show Myths vs. Real Life:Myth #1: Buyers look at 3 homes and make a decision to purchase one of them.Truth: There may be buyers who fall in love and buy the first home they see, but according to the National Association of Realtors the average home buyer tours 10 homes as a part of their search. Myth #2: The houses the buyers are touring are still for sale.Truth: The reality is being staged for TV. Many of the homes being shown are already sold and are off the market. Myth #3: The buyers haven’t made a purchase decision yet.Truth: Since there is no way to show the entire buying process in a 30-minute show, TV producers often choose buyers who are further along in the process and have already chosen a home to buy. Myth #4: If you list your home for sale, it will ALWAYS sell at the Open House.Truth: Of course this would be great! Open houses are important to guarantee the most exposure to buyers in your area, but are only a PIECE of the overall marketing of your home. Just realize that many homes are sold during regular listing appointments as well. Myth #5: Homeowners make a decision about selling their home after a 5-minute conversation.Truth: Similar to the buyers portrayed on the shows, many of the sellers have already spent hours deliberating the decision to list their homes and move on with their lives/goals. Bottom LineHaving an experienced professional on your side while navigating the real estate market is the best way to guarantee that you can make the home of your dreams a reality! Give the Ransom-McKenzie Team a call today to discuss your real estate needs. |

The Civic Side of Homeownership

Are you involved in your community? As Realtors, Charlotte and Connie believe in the value of participating in events and organizations in your home town. The Ransom-McKenzie Team would like to take a moment to share with you this current data which relates to home ownership and civic involvement.

The National Association of Realtors recently released a study titled ‘Social Benefits of Homeownership and Stable Housing.’ The study confirmed a long-standing belief of most Americans:

Today, we want to cover the section of the report that quoted several studies concentrating on the impact homeownership has on the civic participation of family members. Here are some of the major findings on this issue revealed in the report:

Bottom LinePeople often talk about the financial benefits of homeownership. As we can see, there are also social benefits of owning your own home. The City of Riverside is a great place to get out and get involved. Charlotte & Connie are involved in a number of organizations and would be happy to help you find the right group to help you get involved. Give us a call today to discuss your civic involvement at 951-237-2044. |

Calling All Sellers

In Riverside County the real estate world is experiencing a rather severe housing shortage. A healthy real estate market should have about a 5-6 month inventory. Currently in Riverside we have less than a 2.5 month inventory. This means that if you are considering selling your home, now is the time to do it.

The Ransom McKenzie Team is here to help. Before your home hits the market, you’ll want to make sure that it is ready to make a good impression. Remember, you only have one chance to impress a buyer. Here is a helpful infographic with a checklist of ideas for preparing your home for sale:

If you follow some or all of these tips, when you list your home, you’ll be more likely to reach your goal of selling for the best price possible. Most of these items are small projects that don’t take a lot of time or money, but give you a good boost when your home is shown.

The Ransom-McKenzie team is also available to help you as you prepare your home for sale. Call us today at 951-237-2044 for a free evaluation and consultation regarding selling your home.

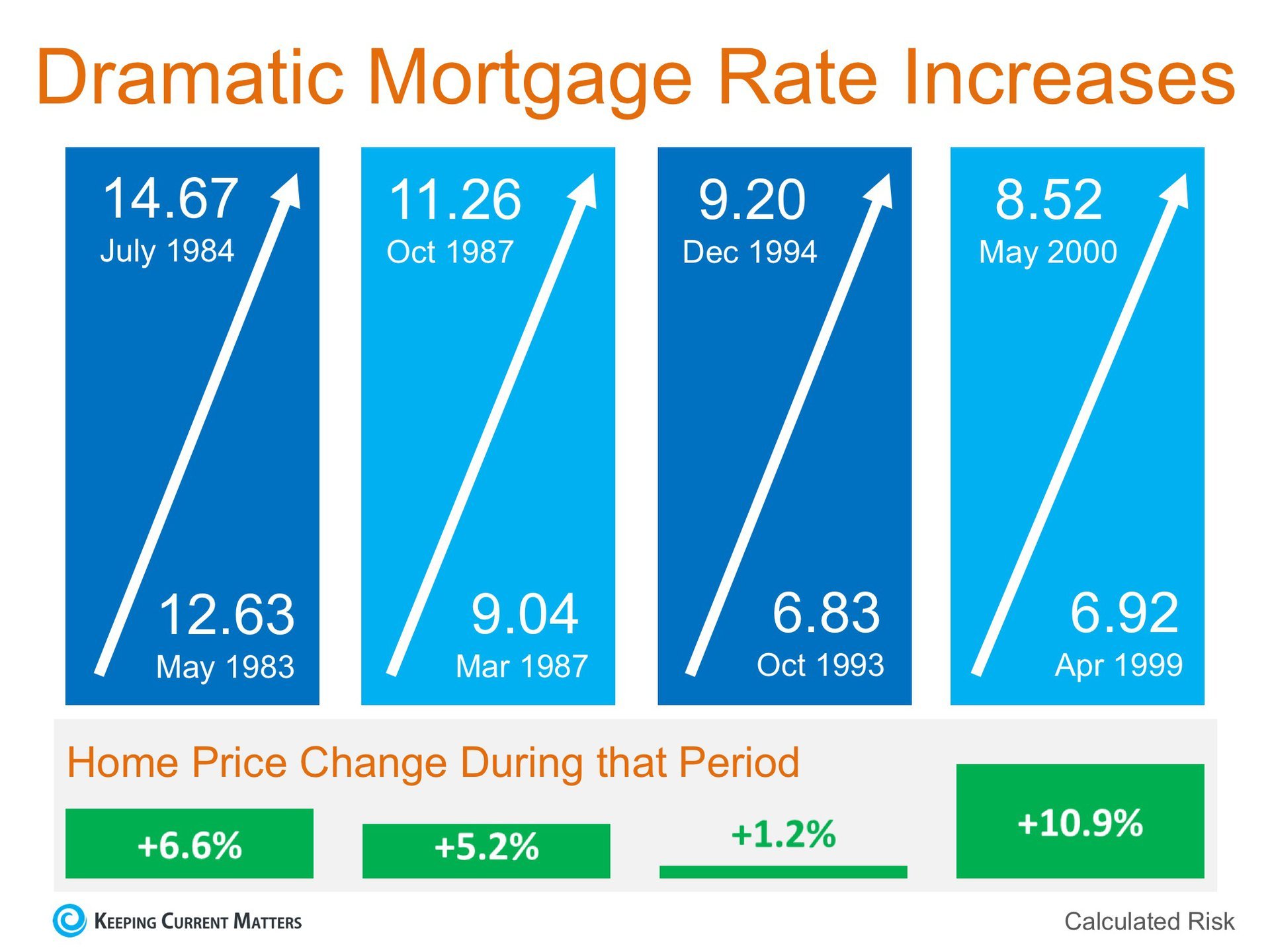

What Do Higher Interest Rates Mean?

There are some who are calling for a decrease in home prices should mortgage interest rates begin to rise rapidly. Intuitively, this makes sense as the cost of a home is determined by the price of the home, plus the cost of financing that home. If mortgage interest rates increase, fewer people will be able to buy, and logic says prices will fall if demand decreases. However, history shows us that this has not been the case the last four times mortgage interest rates dramatically increased. Here is a graph showing what actually happened:

Recently, in an article titled “Higher Rates Don’t Mean Lower House Prices After All,“ the Wall Street Journal revealed that a recent study by John Burns Real Estate Consulting Inc. found that:

The most recent jobs report was strong and the Conference Board just reported that the Consumer Confidence Index was back to pre-recession levels. Bottom LineWe will have to wait and see what happens as we move forward, but a decrease in home prices should rates go up is anything but guaranteed. |