Winter Buyers are Serious

The Ransom-McKenzie Team has been busy already this winter. We’ve been experiencing a high volume of buyers who are ready to buy, now. While winter is often perceived as a down time for real estate, we’re currently seeing trends that indicate this might be a mis-guided perception. Winter buyers are Serious buyers.

Riverside is gorgeous during the winter months!

A recent study of more than 7 million home sales over the past four years revealed that the season in which a home is listed may be able to shed some light on the likelihood that the home will sell for more than asking price, as well as how quickly the sale will close. It’s no surprise that listing a home for sale during the spring saw the largest return, as the spring is traditionally the busiest month for real estate. What is surprising, though, is that listing during the winter came in second!

“Among spring listings, 18.7 percent of homes fetched above asking, with winter listings not far behind at 17.5 percent. While 48.0 percent of homes listed in spring sold within 30 days, 46.2 percent of homes in winter did the same.”

The study goes on to say that:

“Buyers [in the winter] often need to move, so they’re much less likely to make a lowball offer and they’ll often want to close quickly — two things that can make the sale much smoother.”

Bottom Line

If you are debating listing your home for sale within the next 6 months, keep in mind that the spring is when most other homeowners will decide to list their homes as well. Listing your home this winter will ensure that you have the best exposure to the serious buyers who are out looking now! The study used the astronomical seasons to determine which season the listing date fell into (Winter: Dec. 21 – Mar. 20; Spring: Mar. 21 – June 20; Summer: June 21 – Sept 21; Autumn: Sept 21 – Dec. 20).

Orange Roots

The remarkable story of two trees, a pioneer town, and the University of California, Riverside

Riverside’s relationship with the citrus industry runs deep. When the navel orange tree was introduced to our region in 1873, Riverside entered a new era. At one point at the turn of the century, Riverside was the wealthiest city per capita in the United States. Orange Roots, an expansive exhibit now running on the ground floor level of the Rivera Library on the UCR campus, tells the story of how the citrus boom changed our region forever.

This exhibit leads you through the history of the citrus industry in Riverside and how it relates to UC Regents decision to bring a UC campus to Riverside. In 1918 city leaders convinced the UC Regents to build a new Citrus Experimentation Station on the location that is now one of the original campus buildings. It currently houses the Anderson Graduate School of Management.

The pictures and artifacts in this exhibit are beautifully displayed in a custom exhibition set up created to mimic the look of the orange crates of yore. The exhibit includes pictures, orange labels, artifacts and news clippings that document the entire history of the citrus industry and the creation of UCR.

The exhibit is running through January 17th, if you have time during the holidays to go on campus, while the students are on break, it would be well worth the effort.

Millenials vs Boomers

According to the Census Bureau, millennials have overtaken baby boomers as the largest generation in U.S. History. Millennials, or America’s youth born between 1982-2000, now represent more than one quarter of the nation’s population, totaling 83.1 million. There has been a lot of talk about how, as a generation, millennials have ‘failed to launch’ into adulthood and have delayed moving out of their family’s home. Some experts have even questioned whether or not millennials want to move out. The great news is that not only do millennials want to move out… they are moving out! The National Association of Realtors (NAR) recently released their 2016 Profile of Home Buyers and Sellers in which they revealed that 61% of all first-time home buyers were millennials in 2015! The median age of all first-time buyers in 2015 was 31 years old. Here is chart showing the breakdown by age:

If you recall from one of our posts last week, first time home buyers comprised 33% of all buyers in October 2016. The above chart gives you an idea as to how many of those buyers are from the younger generation. Many social factors have contributed to millennials waiting to buy their first home. The latest Census results show that the median age of Americans at the time of their first marriage has increased significantly over the last 60 years, from 23 for men & 20 for women in 1955, to 29 & 27, respectively, in 2015. Those who went to college and took out student loans are finally paying them off, as the terms on traditional student loans are 10 years. This means that a large portion of the generation is making its last loan payments and is working toward saving for a first home. As a whole, the first-time home buyer share increased to 35% of all buyers, up from 32% in 2014. Not all millennials are first-time buyers, they also made up 12% of all repeat buyers!

Bottom Line

Millennials will continue to drive the housing market next year, as well as in the years to come. As more and more realize that owning a home is within their grasp, they will flock to own their piece of the American Dream. Are you ready to buy your first or even second home? Give the Ransom-McKenzie Team a call and we’ll help you through the process.

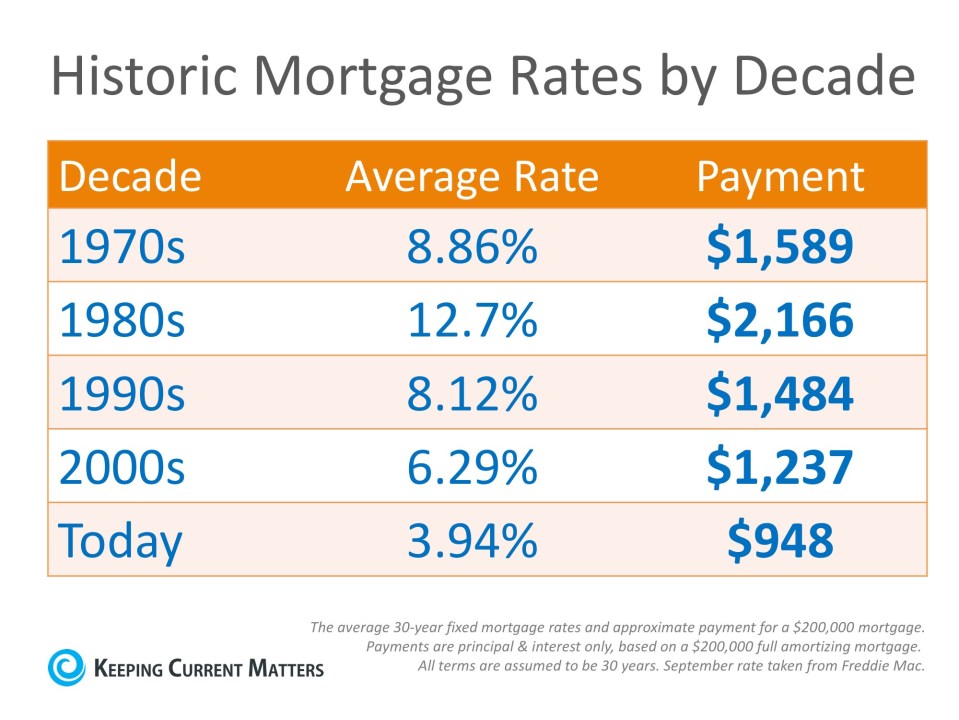

Interest Rates Going UP in 2017

According to Freddie Mac’s latest Primary Mortgage Market Survey, the 30-year fixed rate mortgage interest rate jumped up to 3.94% shortly after the election last month. Interest rates had been hovering around 3.5% since June, and many are wondering why there has been such a significant increase so quickly.

Why did rates go up?

Whenever there is a presidential election, there is uncertainty in the markets as to who will win. One way that this is noticeable is through the actions of investors. As we get closer to the first Tuesday of November, many investors pull their funds from the more volatile and less predictive stock market and instead, choose to invest in Treasury Bonds. When this happens, the interest rate on Treasury Bonds does not have to be as high to entice investors to buy them, so interest rates go down. Once the elections are over and a President has been elected, investors return to the stock market and other investments, leaving the Treasury to raise rates to make bonds more attractive again. Simply put, the better the economy, the higher interest rates will go. For a more detailed explanation of the many factors that contribute to whether interest rates go up or down, you can follow this link to Investopedia.

The Good News

Even though rates are closer to 4% than they have been in nearly 6 months, they are still slightly below where we started 2016, at 3.97%. The great news is that even at 4%, rates are still significantly lower than they have been over the last 4 decades, as you can see in the chart below.

Any increase in interest rate will impact your monthly housing costs when you secure a mortgage to buy your home. A recent Wall Street Journal article points out that, “While still only roughly half the average over the past 45 years, according to Freddie Mac, the quick rise has lenders worried that home loans could become more expensive far sooner than anticipated.” Tom Simons, a Senior Economist at Jefferies LLC, touched on another possible outcome for higher rates:

“First-time buyers look at the monthly total, at what they can afford, so if the mortgage is eaten up by a higher interest expense then there’s less left over for price, for the principal. Buyers will be shopping in a lower price bracket; thus demand could shift a bit.”

Bottom Line

Interest rates are impacted by many factors, and even though they have increased recently, rates would have to reach 9.1% for renting to be cheaper than buying. Rates haven’t been that high since January of 1995, according to Freddie Mac.

The Ransom-McKenzie Team is here to help you through all of the details involved in buying or selling a home. Give us a call today and let us help you!

Home Sales Continue UP

People often ask us how the world of real estate is doing in Riverside. Especially now that we’re closing in on another year, and are looking into next year with a new Presidential administration. We can honestly say that we have had a great 2016, and we are looking forward to more sales in 2017.

The most telling fact in this infographic is that nationwide we’re still experiencing low inventory. While this is driving sales, and has made October the 56th month that we have experienced year-over-year price gains, it has not been pushing prices up as high as one might think. According to the Inland Valleys Association of Realtors Housing Data Report for October 2016 the median sales price in Riverside is $345,000 which is an increase of 5.8% from the previous year. This shows that we are experiencing steady growth in our marketplace.

A nationwide fun fact is that currently 33% of home buyers in October 2016 were first-time home buyers. This shows that the American Dream of home ownership is continuing to be important into the next generation.

The Ransom-McKenzie Team looks forward to assisting our friends and clients with their real estate needs as we look forward to the coming new year. Give us a call if you have a questions about buying or selling a home in Riverside. We Love Riverside!

Downtown Riverside is Growing Up

A vibrant downtown is dependent on creating a good balance of retail and living spaces where people can enjoy not only unique shopping and dining experiences but also can a walkable neighborhood where places are easily accessible. We have watched Downtown as Riverside has become a vibrant economic driver for the city. However, our downtown still lacks spaces where people can live in the Downtown corridor.

The good news is Downtown Riverside will be experiencing a boom of development in the next three years adding over 500 residential, loft style units and nearly 40,000 square feet of unique commercial and office space. The developments include places such as the Mission Inn Lofts, The Stalder Building, Imperial Hardware Lofts, and the Culver Lofts. All of these loft spaces will be centered around our downtown core. Artist renditions of the Mission Inn Lofts and the Imperial Hardware Lofts are shown here:

Bringing more residential living to the heart of Downtown will contribute to the already growing enthusiasm and activity taking place there.

In addition to more residential options downtown, there are also plans to bring more Urban Food venues to Riverside. The 12.000 square foot space adjacent to the Fox Theater is being developed into an Urban Food Hall that will be called the Riverside Food Lab. This location will feature up to 15 vendors and will focus on locally owned stores, no corporate chains allowed. Hopes are to have the Riverside Food Lab up and running in time for the Festival of Lights in 2017. Another unique food venue in the works is Chow Alley. It will feature outdoor dining across from the Historic County Courthouse. The food purveyors here will serve out of cargo style containers, creating a food truck court atmosphere in the heart of the downtown business district.

Check out the City of Riverside’s video about these exciting things coming to downtown Riverside.

There is a lot happening in Riverside! We’re excited to be on the cutting edge of this much-needed development.

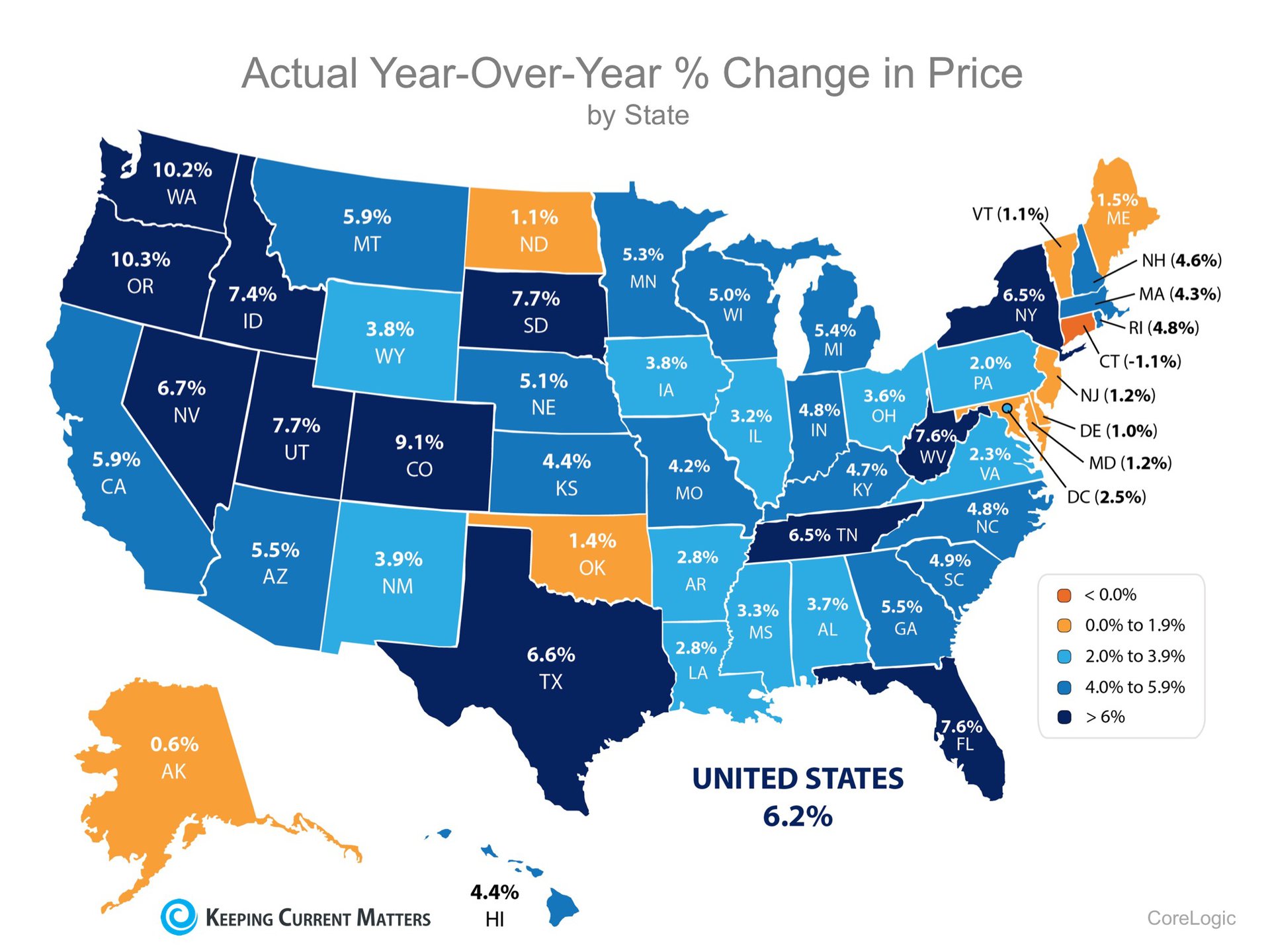

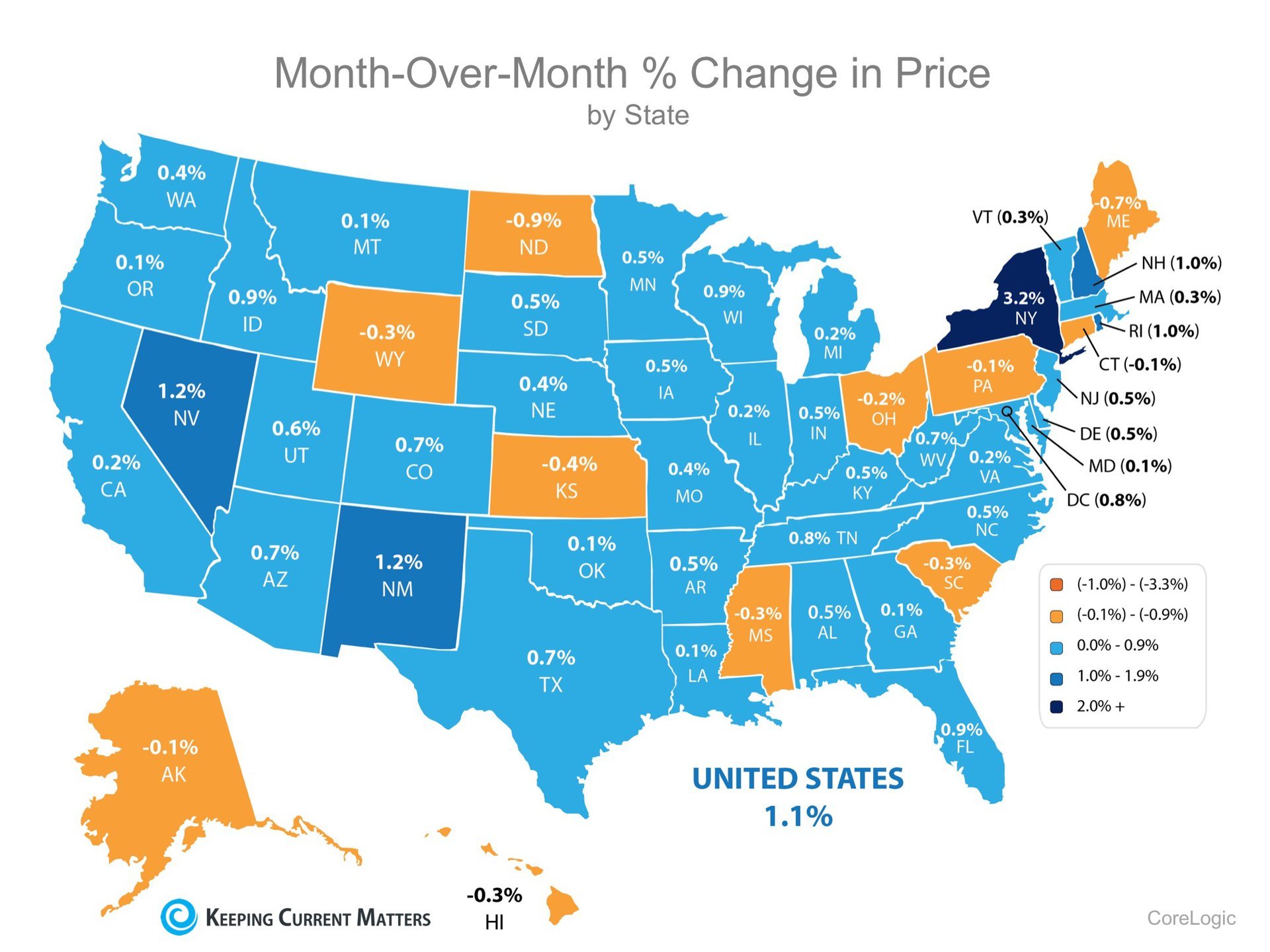

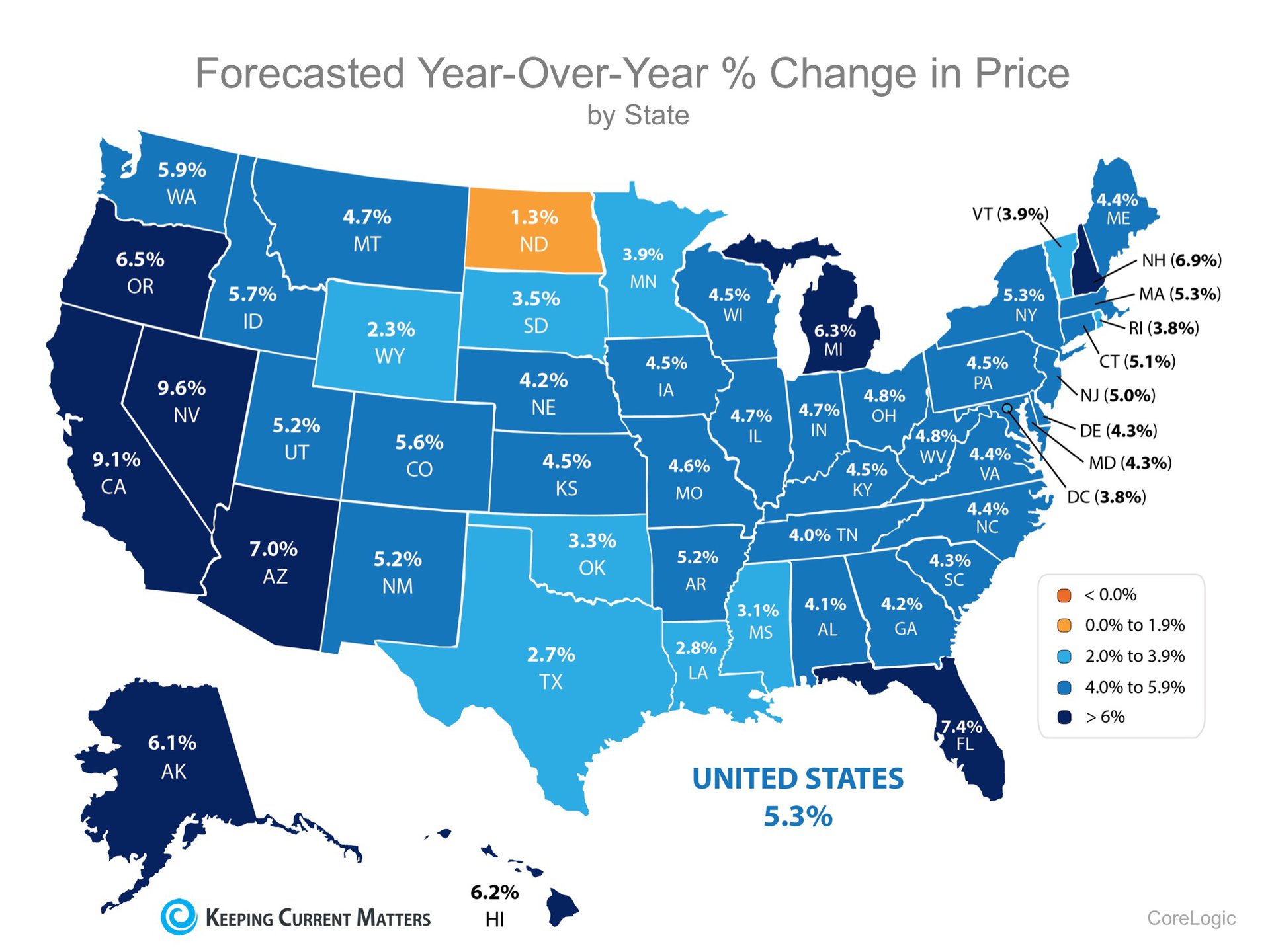

Home Price Update: Where are Prices Going Nationwide?

CoreLogic released their most current Home Price Index last week. In the report, they revealed home appreciation in three categories: percentage appreciation over the last year, over the last month and projected over the next twelve months. Here are state maps for each category:

The Past – home appreciation over the last 12 months

The Present – home appreciation over the last month

The Future – home appreciation projected over the next 12 months

Bottom Line

Homes across the country are appreciating at different rates. In Riverside right now homes are appreciating slightly below the State average at about 5.6% per year. If you plan on relocating to another state and are waiting for your home to appreciate more, you need to know that the home you will buy in another state may be appreciating even faster.

Real Estate is truly a local market. What is happening across the nation, may not necessarily reflect what is happening in your local area. Even markets within a 60 – 100 mile radius can vary drastically. When you’re looking to sell your home, or purchase a new home be sure you meet with a local real estate professional who can help you determine your next steps in your marketplace. The Ransom-McKenzie Team specializes in Riverside. Give us a call today to receive a free evaluation of our local market.

Happy Mother’s Day!

As families celebrate Mother’s Day across the country, I’m preparing for an open house at one of our new listings. I know it seems like it is a bummer to have to “work” Mother’s Day, but somehow it doesn’t seem so bad. Mostly because Connie is my mother!

It is a pleasure and a privilege to be able to work with my mother every day. Not everyone is lucky enough to have such a strong relationship with their mother. It is what makes the Ransom-McKenzie Team strong.

Join us today at our Open House from 1-4pm at 1367 Ransom Road. We look forward to seeing you there. We’ll even have a surprise for the mothers who stop by!!

Check out our video tour of 1367 Ransom Road!

Happy Mother’s Day!!

Sales Price vs. Appraised Value

The Ransom-McKenzie Team is often contacted by sellers who are interested in determining the value of their home. In many instances, they already have a number in mind, they are just looking for us to validate their price. Sometimes we come in with a price at or close to what the seller’s believe to be the value of their home….. other times we don’t. When you are listing your home for sale, choosing the right listing price is an important part of the process for a number of reasons. The most important of those reasons is to make sure that your sales price is going to match the appraiser’s valuation of the home.

The Sales Price

Of course, most sellers want to maximize the value they get for the house. However, the price they set might not be reflective of the other comparable homes in the neighborhood. A recent post on “The Home Story”, a site published by Fannie Mae, explained the difference between the price a seller may get for their home and the value an appraiser might assign the property. The article starts out by stating a fact which is all too familiar to Realtors:

“People tend to view their homes emotionally, and that can become quickly apparent when they decide to sell.”

Nice presentation can positively affect a sale price, but is not the only deciding factor.

That doesn’t mean that the home won’t necessarily sell for that price. A seller can set an asking price and actually have a buyer agree to that price. However, that value may not be necessarily in agreement with what most buyers are willing to pay. For example, one person can view a property, determine it is exactly what they are looking for and well worth the asking price, whereas another person could look at the same property and feel the asking price is too high. Steven Corbin, Director of Valuation in Fannie Mae’s CPM Real Estate division gives an example of this scenario:

“Someone may have driven by the property countless times, and they really want to live in that house. So in reality they may overbid for that property. This would be a situation where the actions of a specific buyer do not represent the actions of a typical buyer.”

The Appraised Price (Market Value)

In their article Fannie Mae describes the process used to determine the value of a home to satisfy their determination of value:

“When a contract is established on a property, an appraised value is determined by a professional real estate appraiser. The appraiser works on the lender’s behalf to determine that value by taking many factors into consideration, including the neighborhood, the value of properties of similar size and construction, and even such things as the type of fixtures on the premises and layout of the floor plan.”

The bank, or lender, wants to know the value that a typical buyer would pay for the property. This price may differ from the agreed upon sales price that the seller and buyer had in the contract.

Selling Your Home Twice

The fact is, when you’re selling your home, you actually have to sell it twice. The first sale occurs when you get the right buyer and all parties agree upon a price. The second sale, which often is the more challenging of the two, is to get the bank, (aka the appraiser), to agree to the same value. If the appraiser comes in with a value that is below the agreed upon sales price, the lending institution might not authorize the mortgage for the full amount a buyer would need to complete the transaction. Quicken Loans actually releases a Home Price Perception Index (HPPI) that quantifies the difference between what sellers and appraisers believe regarding value. The HPPI represents the difference between appraisers’ and homeowners’ opinions of home values. Currently, there is approximately a 2% difference between what homeowners believe their home to be worth and what appraisers value that same home. On a $300,000 sale that would be a $6,000 difference. That could be a challenge that might prevent the home sale proceeding to the closing table.

Bottom Line

In a housing market like the one we’re experiencing in the City of Riverside right now, where supply is very low and demand is very high, home values can increase rapidly. One major challenge in such a market is the bank appraisal. If prices are jumping, it is difficult for appraisers to find adequate comparable sales (similar houses in the neighborhood that closed recently) to defend the price when performing the appraisal for the bank. With escalating prices, the second sale might be even more difficult than the first. That is why we suggest that you use an experienced real estate professional to help set your listing price. Call the Ransom-McKenzie Team today to discuss the value of your home. We’ll be happy to assist you with every step of your real estate transaction.